I finally received a response from the Financial Ombudsman Service this morning about the fiasco I had trying to get a refund to my credit card after MaxJet went bust (which is now almost a year ago) and I had to rebook two flights to Las Vegas.

I’d paid on an MBNA credit card, and their position all along was that I couldn’t have a refund until I’d actually been unable to travel as planned, despite the airline telling customers that they absolutely would not be flying. In other words, I had to wait for each departure date to pass before I’d get my money back.

In this respect, MBNA were true to their word and did post the refunds shortly after the start of each trip. However it meant I was waiting three months for some of it and seven months for the rest and as far as I could tell there was no legitimate reason for them not refunding immediately.

I’d read plenty of accounts online about other travellers getting their money back straight away from reputable banks – including those who had booked on a debit card, which does not carry the same level of consumer protection as a credit card.

So I was having none of it. After I made an official complaint and MBNA stood firm, I took it to the Financial Ombudsman Service.

FOS are slow. I complained on March 10th, after which I had four separate letters telling me they were very busy and would look at my complaint eventually. Which, eventually, turned out to be more than 7 months later.

I’d had all my money back in July but being the stubborn bastard that I am, I told FOS that I still wanted them to process the complaint.

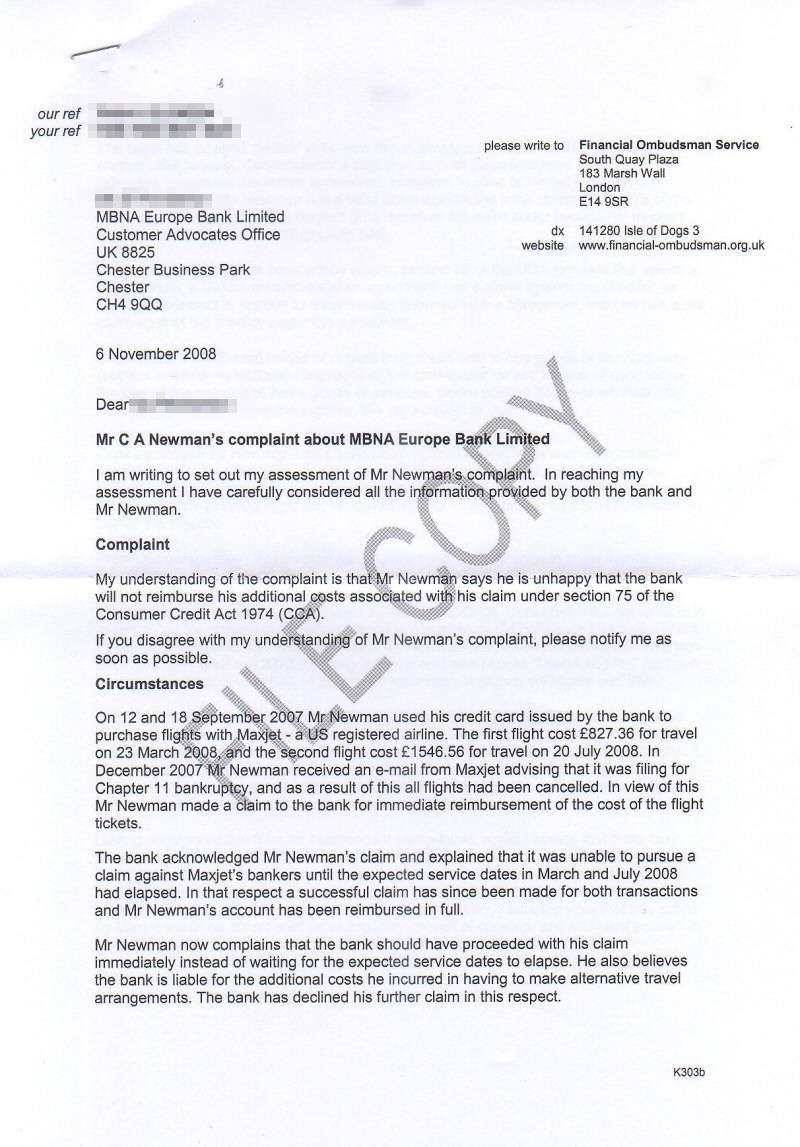

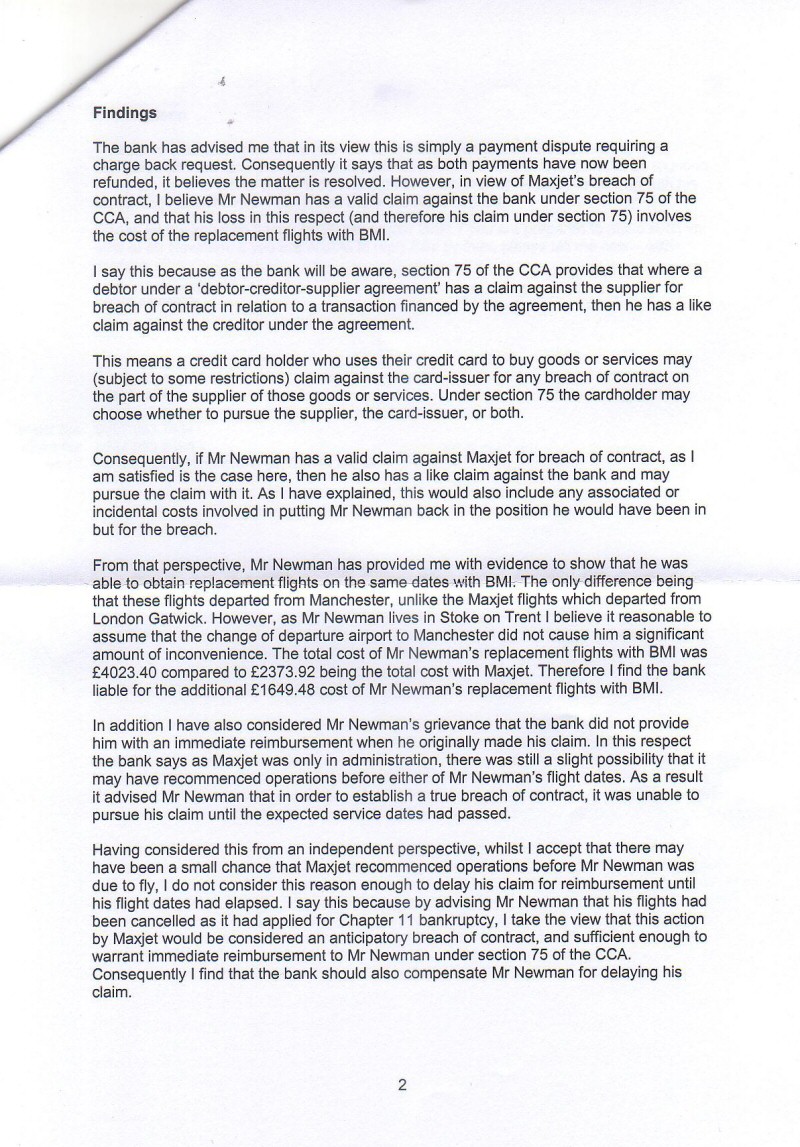

I had also suggested that MBNA should still be liable for the difference in cost because of the more expensive flights I booked as an alternative under the Consumer Credit Act, which they have tried so hard to pretend doesn’t apply to them.

It looks like it was worth the wait. The FOS adjudicator has sided with the law, rather than MBNA’s interpretation of "MasterCard guidelines".

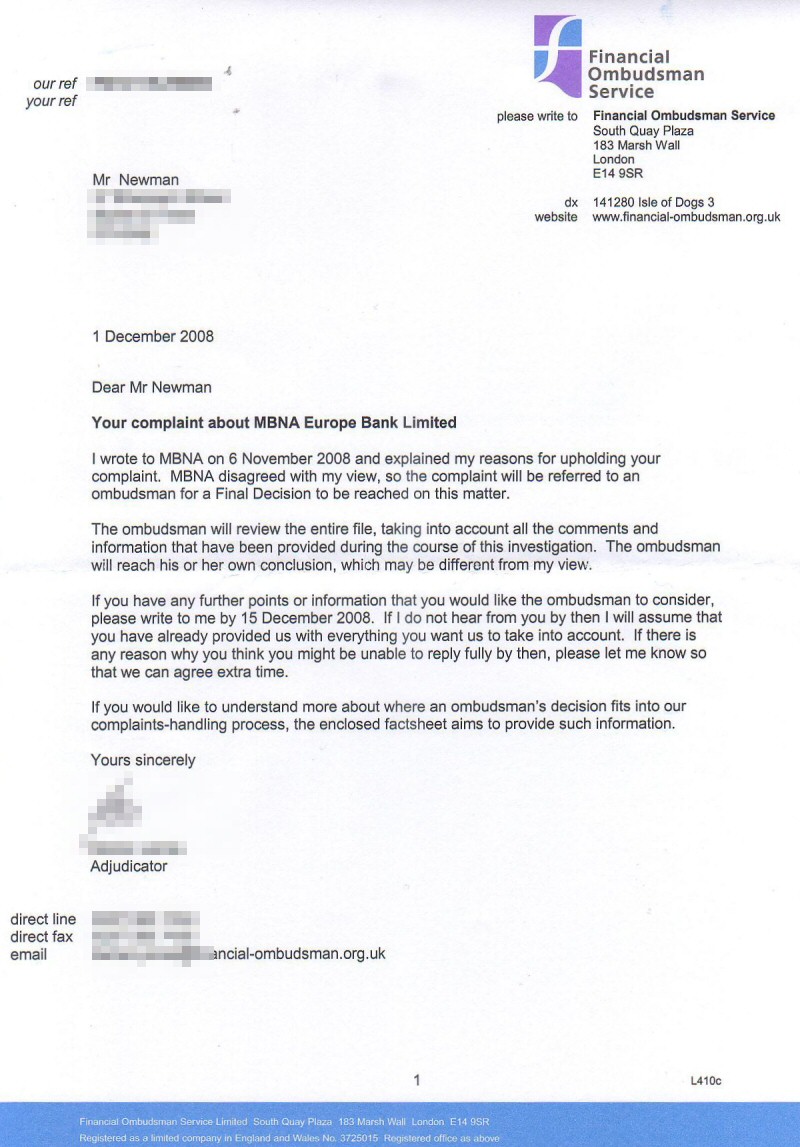

Although they made an adjudication last month I only received a copy of it today because MBNA have (predictably) rejected this suggestion that they pay me money. So it’s now being referred to an actual ombudsman, rather than a henchman, who will make a legally-binding decision.

This could still take months, but I don’t care.

It’s super satisfying (assuming the ombudsman does reach the same conclusion) because if MBNA had simply given me a refund straight away (like they were meant to) I almost certainly wouldn’t have bothered doing anything to recover the cost difference.

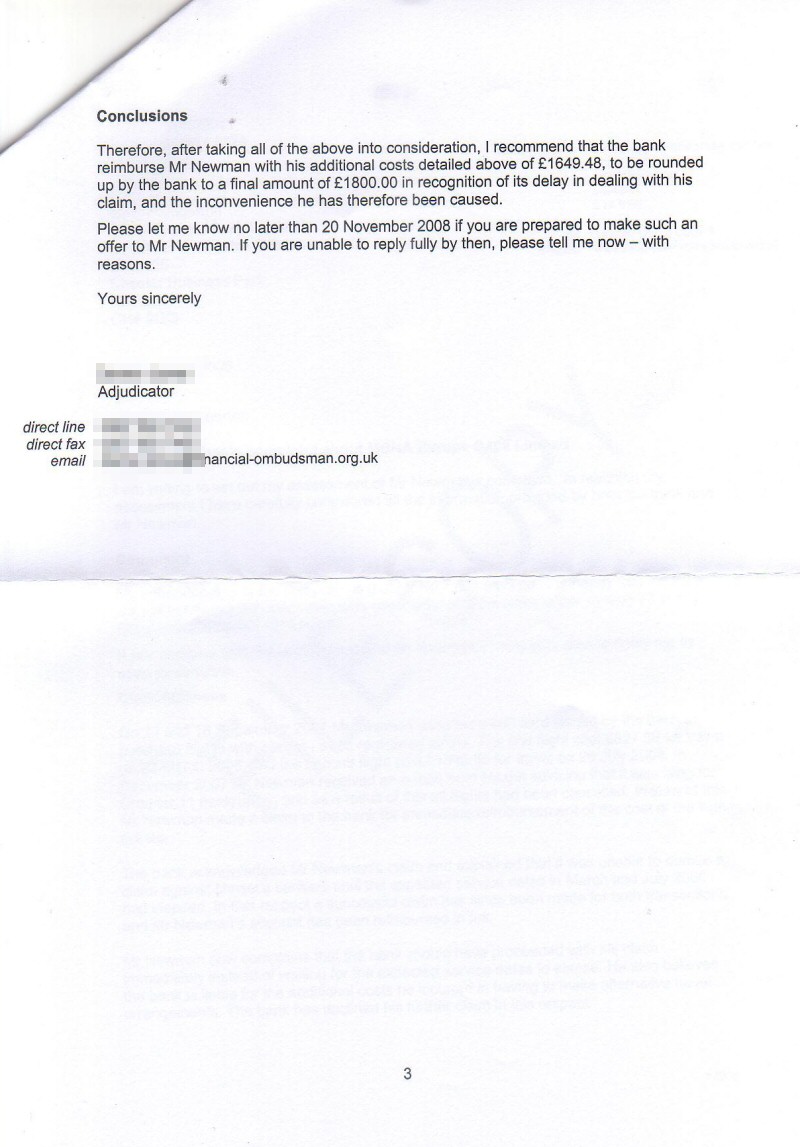

The adjudicator also decided I should have the amount rounded up by about £150 as compensation for having to wait for the refund. Which is nice.

The only reason I still have this credit card is because I can earn BMI miles on everything I spend, but with the Lufthansa takeover looming and the possibilty of Diamond Club getting swallowed up by their programme as well as the cancellation of BMI’s transatlantic flights next year, I’ll probably be doing away with it soon.

Sadly, MBNA won’t miss me as a customer. I’ve never paid a penny of interest on that card.

Anyway, if you’re interested in seeing what FOS had to say about these shenanigans, here are copies of the letter I had today and the adjudication sent to MBNA (click to enlarge).

Comments